Overview

2025 is set to be one of the busiest years on the Hill when it comes to tax policy. With the looming sunset of certain provisions of the Tax Cuts and Jobs Act (TCJA) and other key phaseouts, we expect there to be an uptick not only in rhetoric but also proposed bills in 2025. Not all bills will have a real shot at passage—in fact, many will simply be “messaging” bills put forth for political purposes. Taxpayers are therefore left with the task of understanding how to plan and strategize their tax positions in a landscape that is far from certain. This guide attempts to address this uncertainty by providing readers with a background knowledge of “how things work” on the Hill. Regardless of the bills in play at the time, understanding indicators of a bill’s viability paired with an understanding of those leading the charge of tax legislation can more fully inform taxpayers’ business decisions. Forvis Mazars hopes this guide arms you with the tools to navigate an otherwise confusing time and is prepared to strategize with you and your business given the tax landscape at hand. Please note this is not a partisan document.

- Viability of Legislation: How to Tell What’s “Real”

- Congressional Tax Leader Profiles

- Looking Forward: Sunsets & Predictions for 2025 Legislation

Viability of Legislation: How to Tell What’s “Real”

According to the Constitution, all tax legislation must originate in the House of Representatives. Although tax bills are also introduced in the Senate, tax bills must originally pass in the House, where is it also procedurally easier given the availability for extended debate, extraneous amendments, and the potential for filibuster within the Senate. Regardless, the two main congressional tax writing committees—the House Committee on Ways and Means and the Senate Committee on Finance—greatly influence (if not control) the progress of tax legislation. Inevitably, the party in the majority in each chamber plays a huge factor in what is considered and ultimately passed as law—making it important to understand the players in Congress today when considering upcoming legislation. This section of FAQs addresses questions that provide further background as to the overall processes that affect a bill becoming a law, and in turn attempts to provide further clarity into a proposal’s viability when making your own business decisions accordingly.

What are good indicators that a bill has a better chance for passage?

Sponsor(s) of the bill

If the sponsor(s) of a bill has a longer history of involvement in tax policy, i.e., is a member of one of the congressional tax-writing committees, this could be a good indication for the bill’s chances. If instead they are relatively new to Congress or not a member of one of the tax-writing committees, the bill could be more of a building block for the sponsor’s resume instead of a real contender for future movement.

Number of co-sponsors of the bill

In general, the more co-sponsors on a bill the better, particularly once again if those co-sponsors sit on the tax-writing committees. This has the potential to reflect the overall support of the bill.

Party affiliation of co-sponsors

Regardless of the number of co-sponsors, it might signal a lack of bipartisan support if the co-sponsors are exclusively of one party. Depending on the makeup of the House or Senate at the time, having at least some cross-party support could prove crucial to a bill’s passage.

Hearings on the bill

Hearings allow for feedback from external parties, such as industry experts—known as “witnesses”—to provide feedback. However, committee markups are needed to advance a bill from the committee to the broader floor. Yet again, the committee chair is responsible for determining which bills go into markup and will likely not do so unless the chair is confident that it will pass, i.e., have majority support. Therefore, a good indicator of whether a bill will pass is whether it enters markup.

Similar bill present in the other chamber

A bill passing one chamber of Congress does not necessarily provide insight into the likelihood that it will also pass the other chamber. If, however, similar bills are present in both chambers, it may be more likely that there is broad support for the topic.

Can bills from 2024 or earlier still be considered in 2025?

Each “Congress” lasts for two years (two “sessions”), and only those bills proposed and passed within a Congress can become law. The current Congress (the 118th Congress) spans calendar years 2023 and 2024, meaning any bills proposed but not passed by the start of 2025 would need to be re-proposed by the 119th Congress to become law.

Current Event Implications: The Tax Cuts for Working Families Act (“the Bill”) was proposed originally in 2023, meaning it is a bill of the 118th Congress. Despite the House’s passing of the Bill, the Senate voted against starting debate on the Bill through what is called a “cloture motion.” While technically possible for portions of the Bill to be passed in the lame duck session following the November 2024 election, consultants of Forvis Mazars believe consideration is at best uncertain and highly dependent on the results of the November elections. As a result, it falls to those in the 119th Congress to determine what portions (if any) of the Bill would be incorporated into “new” legislation being proposed in 2025 or 2026. 2025 is set to be a uniquely busy year for Congress given the upcoming sunset of many tax provisions, including those implemented by the Bill. Therefore, while you may hear rhetoric that the Bill is “dead,” it does not necessarily mean that no portion will become law in the near future.

How do the House and Senate differ in structure and process?

Key comparisons of each chamber of Congress are as follows:

| House | Senate | |

|---|---|---|

| # of Members | 435 | 100 |

| Terms | 2 years | 6 years |

| Tax Committees | House Committee on Ways and Means | Senate Finance Committee |

| Methods for Passage |

| For passage, simple majority. Procedurally:

|

Which committees and subcommittees are focused on tax?

Some of the key committees and subcommittees focused on tax and tax policy are:

- House Ways and Means Committee

- Ways and Means Subcommittee on Tax Policy

- Senate Finance Committee

- Senate Finance Subcommittee on Taxation and IRS Oversight

- Joint Tax Committee

What is the Joint Tax Committee? Are they influential?

The Joint Tax Committee (JTC) is neither a subcommittee under the House nor the Senate. Instead, it is comprised of members from both chambers and is used as a highly trusted group of individuals focused on supporting tax legislation. In fact, the meetings between JTC members and members of Congress are confidential, allowing for a more open and honest venue for working through complex topics. JTC staff is comprised of a large number of tax lawyers, accountants, economists, and other specialists who work on a non-partisan basis on behalf of the Congress. According to its website, the JTC is involved in the following:

- “Assisting Congressional tax-writing committees and Members of Congress with development and analysis of legislative proposals;

- Preparing official revenue estimates of all tax legislation considered by the Congress;

- Drafting legislative histories for tax-related bills; and

- Investigating various aspects of the Federal tax system.”

Do committees play a role in deciding which bills are considered, and when?

Yes. After the Speaker refers the bills to the appropriate committee, the chair of the committee sets the timeline and priority of bills for consideration. Chairs also determine which bills will have a hearing or go through committee markup. The chairs are of the same party that is in the majority, which makes congressional elections even more important. Further, the makeup of committees usually mirrors the broader composition of the chamber. Therefore, if the House is majority Republican, so too will be the House Ways and Means Committee—a fact that helps to predict what proposals will make it to the floor and ultimately become law. Congressional leadership can, in many instances, bypass the committee process to bring tax legislation directly to the floor of their respective congressional chambers.

How do the committee processes vary between the House and Senate?

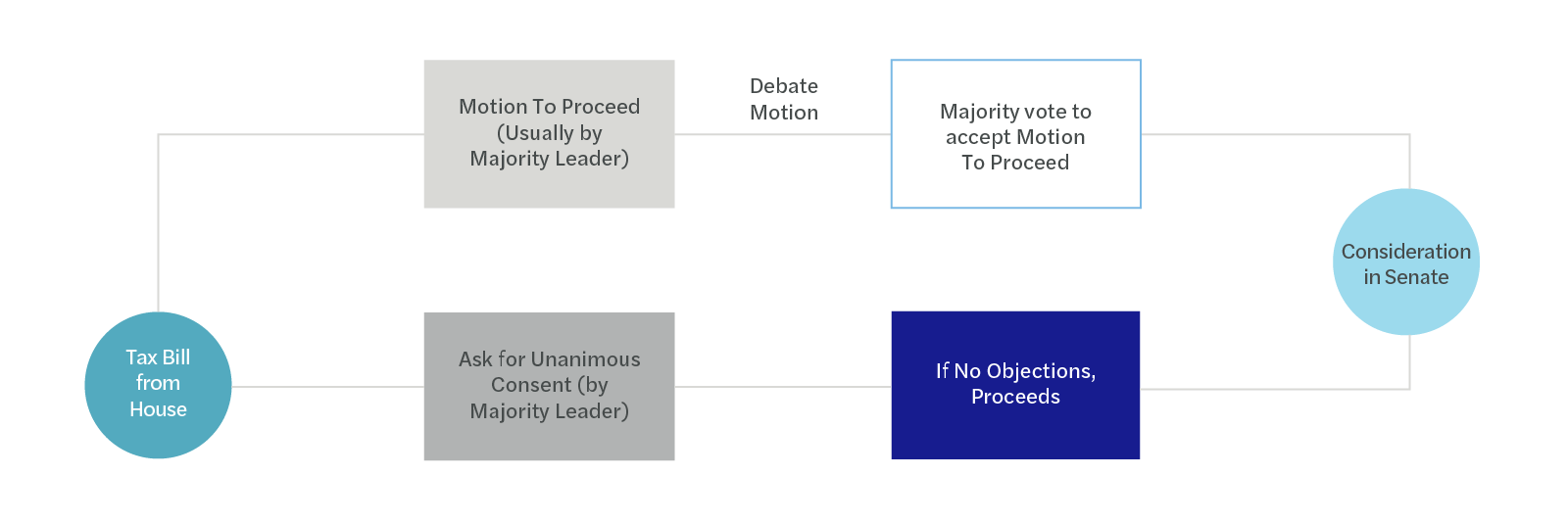

A visual of the House committee process is depicted below:

- Tax Bill from House

- Motion to proceed (Usually by Majority Leader)

- Debate Motion

- Majority vote to accept Motion to Proceed

- Ask for Unanimous Consent (by Majority Leader)

- If No Objections, Proceeds

- Motion to proceed (Usually by Majority Leader)

- Consideration in Senate

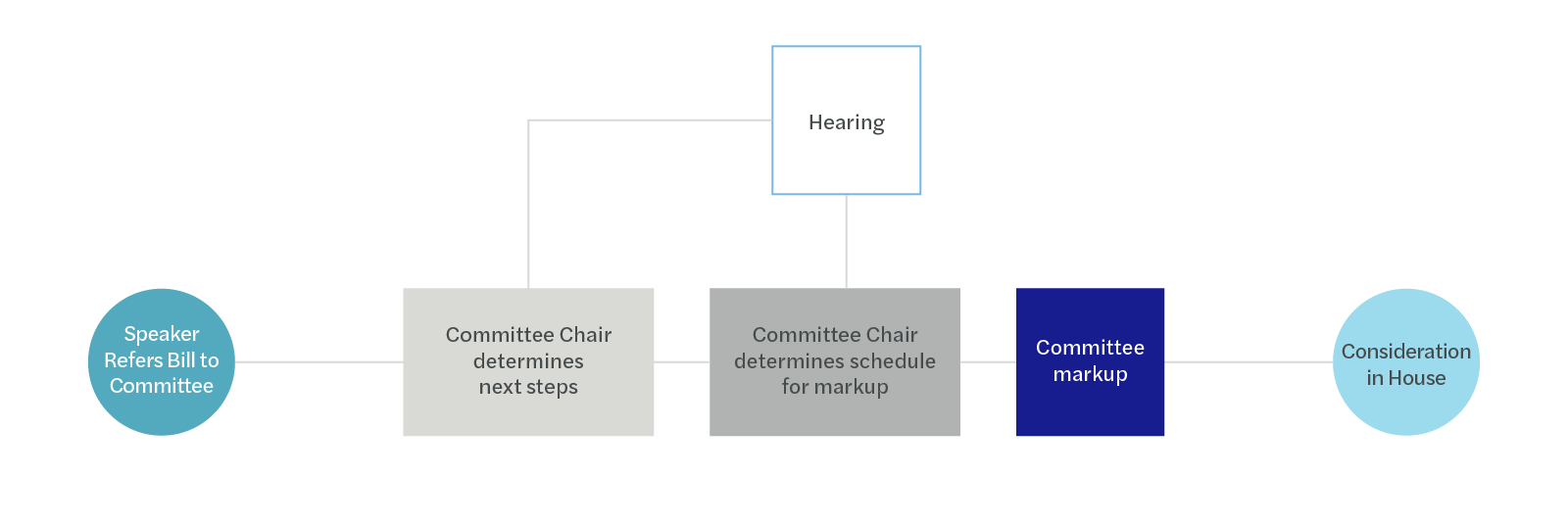

In the Senate, the committee process is a bit more complicated, as depicted below:

- Speaker refers Bill to Committee

- Committee Chair determines next steps

- Hearing

- Committee Chair determines schedule for markup

- Committee markup>

- Consideration in House

Is it generally quicker for a bill to pass the House or the Senate?

The House procedures for bill consideration generally result in a quicker passage of bills than the Senate. Tax bills are generally not subject to amendment on the House floor, which avoids what are often referred to as “Christmas Tree Bills” in the Senate. “Christmas Tree Bills” are dubbed as such given the number of unrelated “pet project” proposals Congressmen may try to add into a larger bill, much like an ornament on a Christmas tree.

Is it true that individual senators have more relative “power” to influence legislation passage than House representatives?

Senate consideration can be lengthy and can even be a dead end for much legislation due to the availability of a filibuster and lack of restrictions on amendments. Given the ability for debate and amendment, it is possible that individual senators may wield more power and influence over specific legislation.

What are some options to avoid filibuster or excessive amendment and debate in the Senate?

Cloture Rule

As long as the cloture motion is signed by 16 senators and 60 of the senators agree to the cloture motion, then debate can be limited to 30 hours and amendments are limited as defined. To pass, only a simple majority is required at this point. The 60-vote requirement for the cloture motion is the real hurdle for this process to be successful. If a cloture motion is introduced, it is normally with the informed foresight that there will be enough support for both the motion and the bill in general. Once again, for more controversial topics (like tax bills), this brings the importance of a supermajority to the forefront.

Unanimous consent agreements

If no senator objects, these agreements outline a procedure and limitations on the Senate’s hearing of the bill. These function similarly to Special Rules in the House.

Reconciliation bills

Practically speaking, reconciliation bills are unlikely unless the President, House, and Senate are of the same party.

Reconciliation bills, unlike non-reconciliation bills, only need a simple majority for consideration and passage in the Senate. However, not all bills can be considered under the reconciliation process. Reconciliation bills can be used for changes in “spending, revenues, and/or the federal debt limit.”1 Only mandatory spending—and not discretionary spending—can be considered via reconciliation, excluding items otherwise considered in the appropriations process.

The Byrd Rule provides a “check” to the reconciliation process. Essentially, the Byrd Rule is akin to the “germaneness” rule in the House—it stops senators from adding provisions to the reconciliation bill that aren’t related to its core purpose. There are certain guidelines about what would be considered extraneous according to the Byrd Rule.

Why is there so much discussion about funding for TCJA extenders and other 2025 legislative priorities? Said another way, why not just pass them and incur more debt?

The current deficit situation has placed significant pressure on funding future tax relief and spending bills. Whereas some members of Congress believe that tax relief bills actually fund themselves through increased economic growth, more conservative members are insisting on paying for any future tax relief bills.

Do tax bills need to be attached to another legislative “vehicle” or can they also pass on a standalone basis?

Tax bills can pass on either a standalone basis or attached to another legislative vehicle. In recent years, there have been fewer tax bills passed on a standalone basis because of narrow majorities in Congress. It is arguably easier for congressmen and congresswomen to support a tax bill attached to a broader vehicle. If the vehicle has less controversial topics more easily agreed to, it may be more palatable to pass tax legislation as a part of the larger bill.

Does the appropriations process affect the timing of when tax legislation may pass in 2025?

Probably not. The biggest factor for the timing of tax legislation is the results of the 2024 election, and the extent of a majority by either party in Congress’ chambers. Legislative consultants of Forvis Mazars have indicated that there will likely be fewer messaging bills entering markup in 2025, considering the enormity of the task at hand (TCJA’s sunsets and other phaseouts). There will be many hearings, which will inevitably affect the timetable of tax legislation as well. A fall continuing resolution to temporarily fund the government past September 30, 2024 may emerge as a potential legislative vehicle to carry a tax title, such as the 2024 tax relief bill previously passed by the House.

Congressional Tax Leader Profiles

Leaders of various tax committees and subcommittees have real influence over the progress of tax legislation. Forvis Mazars gathered profiles as a “quick look” into some of these leaders. Download the PDF below to view their historical sponsorship, publicized priorities, and related news stories that may help to predict where they could stand in 2025 legislation negotiations.

Looking Forward: Sunsets & Predictions for 2025 Legislation

Legislators on the Hill will be busy in 2025 with tax proposals. Aimed at dealing with the TCJA sunsets, other phaseouts, and the priorities of a new president, some have begun referring to 2025 as the “Tax Super Bowl” in Congress. This section summarizes the sunsets related to TCJA and other phaseouts, and how you might plan for them.

If TCJA is not extended, what changes would taxpayers see in 2026?

The following outline changes effective beginning in 2026 if Congress takes no action.

| Topic | Current State | After Sunset |

|---|---|---|

| Section 199A-QBI | 20% Deduction | No Deduction |

| Section 174 Capitalization | 5-year capitalization for domestic and 15-year capitalization for foreign | Capitalization remains |

| Estate and Gift Tax Exemption | $13.61M/individual, $27.22M/MFJ couple | Estimated $6-7M/individual, indexed for inflation |

| Tax Rate Changes |

|

|

| Personal Exemptions, Deductions, and Limitations |

|

|

| SALT “Cap” | $10,000 deduction “cap” | Limited by AGI, but no dollar “cap” |

| Mortgage Interest Deductibility | $750,000 threshold (MFJ) | $1M threshold (MFJ) |

| Miscellaneous Itemized Deductions | Nondeductible | Deductible in excess of 2% AGI |

| AMT | $133,300 MFJ exemption, phase-out at $1,218,700 MFJ | $120,700 MFJ exemption, phase-out at $160,900 (to be adjusted for inflation) |

| GILTI | 10.5% | 13.125% |

| BEAT | 10% | 12.5% |

| FDII | 13.125% | 16.4% |

What would be an individual’s tax impact of a full TCJA sunset?

While many of the above provisions have been beneficial to companies and individuals alike since passage, the estimated impact of extending all TCJA provisions comes in at a $4 trillion price tag. That being said, according to the Tax Foundation,2 the following depicts how individuals in various income positions would fair if TCJA were not extended at all:

| Filing Position | Tax Impact |

|---|---|

| Single, No Dependents | $2,623 increase |

| Single, 1 Dependent | $3,870 increase |

| Married Filing Jointly, No Dependents | $1,867 increase |

| Married Filing Jointly, 2 Dependents | $2,277 increase |

What other phaseouts should businesses consider?

Arguably the most impactful non-TCJA phaseout is bonus depreciation. At the end of 2026, unless a change is made, bonus depreciation will be reduced to 0%. Undoubtedly this will increase those pursuing Section 179 expensing as an alternative and will usher in new strategies surrounding depreciation. Purchasing property will no longer result in a first-year windfall to taxpayers, which has the potential to impact negotiations of everything from asset sales to entity transactions.

Other business phaseouts include:

- Work Opportunity Tax Credit (WOTC): Available to taxable and tax-exempt employers alike, this incentive allows for a credit for those hiring workers in WOTC targeted groups through December 31, 2025.

- New Markets Tax Credit (NMTC): Available through December 31, 2025, the NMTC was established to support investment in certain communities. Bills have been proposed recently to adjust and make the NMTC permanent.

- Controlled foreign corporation (CFC) Look-Through Rule: After having been extended repeatedly in the past, this CFC Look-Through Rule is once again due for expiration.

What strategies have Republicans publicized as possible funding mechanisms for their extension of TCJA?

Another question is to what extent, and from where, the Republicans may try to fund the extension of TCJA provisions to counteract the $4 trillion price tag. As of July, Donald Trump has suggested several ideas for this purpose, some of which will undoubtedly be met with Democratic pushback. First is the repeal, or at least partial repeal, of the IRA. Regardless of the policy sentiments of those in the Republican party, the IRA is estimated to cost around $780 billion through 2031 according to the Brookings Institute.3 However, the IRA clean energy credits have benefited many states with Republican control, so repealing the entirety of the IRA is not seen as likely.

That being said, a big chunk of the IRA allocation was the $80 billion allocated for additional funds to the IRS. Many Republicans have expressed concerns over IRS data security, responsiveness, and ability to catch bad actors. However, they have continually targeted the IRS funding as an opportunity to offset their policy priorities elsewhere.

Other possible funding sources could be a two-fold policy “win” for Trump—a 10% tariff on foreign imports and a 60% tariff on Chinese imports. Not only would this support his initiative to incentivize domestic producers, but it could also help to fund his TCJA extender efforts.

Lastly, it is possible that the infamous “SALT cap” gets extended as part of this funding effort. While counter to some of Trump’s initiative to cut taxes, the implementation of the SALT cap has seen many states implement pass-through entity tax (PTET) workarounds that offset the burden at least to some extent. This may serve as a bargaining chip between Democrats and Republicans moving forward to 2025 negotiations.

What is Congress doing now in preparation of the 2025 tax legislative season?

House Republicans established “tax teams” focused on various topics that are tasked with collecting and reviewing commentary from the public. Open through October 15, interested parties could submit comments for consideration by the team through a comment portal. These teams are as follows:

- American Manufacturing

- Working Families

- American Workforce

- Main Street

- New Economy

- Rural America

- Community Development

- Supply Chains

- U.S. Innovation

- Global Competitiveness

There are reports that the Senate Committee on Finance will also utilize a similar tax team or tax working group mechanism, although no process has yet to be formally announced.

Would you expect the 2024 Tax Cuts for Working Families Act proposal to influence legislation in 2025?

It is possible that portions of the Act would be incorporated into future proposals. Section 174 expensing was implemented as a part of TCJA, so whether the capitalization requirement is again negotiated as a funding tactic for 2025 legislation is yet to be seen. Affordable housing has been vocalized as priorities of both presidential candidates, so it is likely that a tax package would include at least some provision to support this topic. While not a part of TCJA, the bonus depreciation phaseout was publicized as one of the “big three” proposals in the Tax Cuts for Working Families Act, gaining bipartisan support across the board.

What should I be doing now in anticipation of these possible changes?

Reach out to your Forvis Mazars tax professional to discuss your situation and what (if anything) should be done at this time. Among others, we expect common considerations to include 2025 gifting in anticipation of the estate and gift tax exemption change, possible entity structure changes, and deferral of R&D expense incursion. Considering the uncertainty with the current political environment, it may be most prudent to continue monitoring bill progression prior to making any changes for your or your business’s tax plans.

This FORsight reflects information accurate as of the date this piece was published. Forvis Mazars acknowledges that some of this information may change over time, therefore readers should consider whether the enclosed information has been superseded or modified by any developments following November 20, 2024. For updates and similar content, be sure to subscribe to our FORsights mailing list or visit our WNTO website.